Diesel Markets Don’t Lie: Structural Shocks, Policy Mistakes, and What the Data Reveal

My newly published co-authored paper on diesel prices, structural breaks, and how misreading energy markets leads to costly policy failures.

Hello friends!

How resilient is the diesel market when the government keeps distorting prices?

My latest peer-reviewed, co-authored research, published in Oil, Gas & Energy Quarterly, delves deeply into this critical question. In this post, I break down what the data show, how the market adjusts (or doesn't), and what policymakers need to stop doing if they want to help working families and truckers, rather than hurting them.

Back to Basics: Supply, Demand, and Diesel

Diesel isn’t just another fuel—it’s the backbone of freight, farming, construction, and everyday logistics in America. When diesel prices spike or remain artificially volatile, the costs ripple across the economy, crushing families and small businesses.

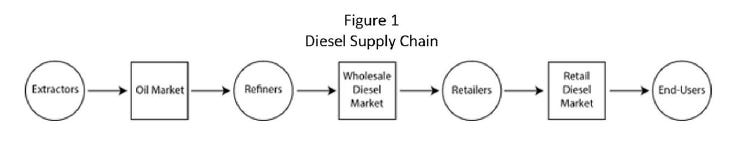

In my newly published paper, “Structural Breaks and Longrun Adjustment in the Diesel Fuel Market” (with co-authors Chris Douglas, Mark Tuttle, and Don Bumpass), we investigate how diesel fuel prices respond to long-term disruptions and whether markets eventually return to their previous trends.

Key Finding:

Yes, diesel markets adjust over time—but not always smoothly. We find evidence of multiple structural breaks, points at which the usual relationships between variables (such as crude oil prices, supply shocks, and regulations) shift permanently.

That means policy shocks, such as regulatory mandates, price interventions, or geopolitical disruptions, don’t just cause temporary price spikes. They can change the market's behavior altogether.

Why This Matters Now:

The government has an annoying habit of thinking markets are machines to be fine-tuned. But markets adapt—and sometimes they break. Diesel is a textbook example.

🔹 Diesel prices remain elevated and volatile despite some declines in crude prices.

🔹 Regulatory burdens—especially environmental mandates—have permanently raised costs on refiners.

🔹 Tariffs on global energy trade, like those pursued under the Trump administration and expanded now, distort input prices and ripple through to diesel.

🔹 And bad monetary policy—whether through ultra-low interest rates or excessive Fed balance sheet expansion—inflates energy costs indirectly through demand misalignment.

Policy Implications:

We need less tinkering, more trust in price signals, and a better understanding that policy mistakes can leave lasting damage. Markets can adjust, but only if left free to do so. As our research shows, diesel prices don’t return to trend automatically, especially not when heavy-handed policy keeps shifting the goalposts.

My Take:

This paper is another reason why the government shouldn’t try to micromanage energy markets. Structural breaks don’t just happen—they’re often caused by policy itself. Politicians and central bankers would be wise to stop piling on distortions and let competition, innovation, and supply chains do what they do best.

Want prosperity? Let markets price energy. Stop the regulatory chokeholds. Scrap distortive tariffs. Shrink the Fed’s role in distorting credit and commodity prices.

Final Thought:

I’m proud to share this new research with both my academic and policy audiences. Diesel may not make headlines every day, but understanding it is crucial to grasping prices, supply chains, and how government failure can lead to market failure. If we get diesel right, we can get a lot else right, too.

Let’s keep pushing for policies that allow people—not bureaucrats—to prosper.

Message me if you’d like me to send you a PDF of the paper. Check out my other publications here. Reach out if I can be of service to you. Please share with your network and as a note on Substack. Thanks!

The obiter dicta on the Fed does not strengthen your otherwise perfectly sensible POV on energy market interventions. :)