Healing Washington’s Spending Binge

A 3 percent deficit target is better than drift, but a hard spending limit is the real fix

Hello friends,

When even Washington starts admitting the math no longer works, you know the problem is serious.

That is why US House Budget Chairman Jodey Arrington’s recent remarks matter. He said plainly that the old fiscal playbook is broken. In 2017, he noted, the savings needed to balance the budget in 10 years were about $6 trillion. Now they are closer to $16 trillion.

He is right that the country is in dangerous territory. He is right that deficits and debt relative to GDP matter. And a 3 percent deficit-to-GDP framework is certainly better than the denial and drift we have now.

But let’s be honest about the deeper problem. Washington does not have a tax revenue problem. It has a spending problem. That is the whole ballgame.

Spending Comes First

As I have noted in my work on Responsible State Budgets Across the U.S., government spending is the problem because it comes first. Debt comes after. Inflation comes after. Pressure for higher taxes comes after.

Politicians spend too much, then act surprised when the bill shows up. And the bill is here.

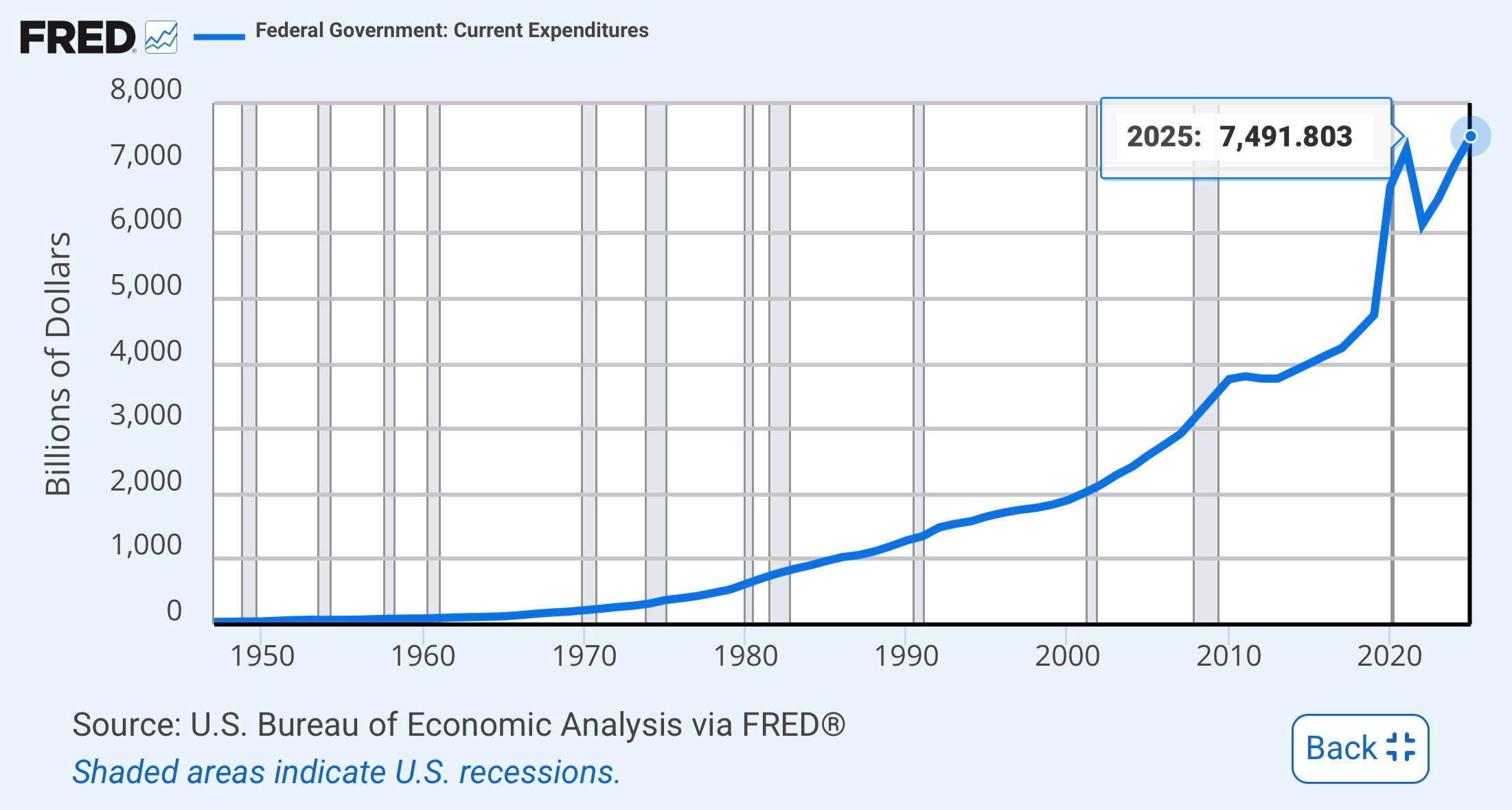

Federal spending was $4.8 trillion in 2019. By fiscal year 2025, it had climbed to $7 trillion. That is not normal growth. That is a spending binge.

My broader budget work shows the same pattern over a longer stretch: from 2015 to 2024, federal spending rose 88.0 percent, while population growth plus inflation rose just 27.6 percent. Had Congress simply restrained spending to that sustainable benchmark, Washington would have spent $2.2 trillion less in 2024 alone.

Why the Rule Matters

That is why I recommend a strict spending limit rather than a deficit ratio.

A 3 percent deficit target can tell you something is wrong. It is a useful warning light. But it does not tell you how Washington gets there.

Politicians can chase a lower budget deficit through higher taxes, rosy assumptions, gimmicks, or inflation doing some of the work for them. That may improve a ratio on paper while leaving the federal government too large and the private economy too burdened.

A hard spending limit tied to population growth plus inflation is better because it goes straight at the source of the problem: overspending. It should also be treated as a ceiling, not a target. That distinction matters more than most people realize.

Friedman and Alesina

Milton Friedman understood it well. He warned that the true burden of government is what it spends, not merely how it is financed. Higher taxes do not solve the real problem if they simply make room for higher spending later.

That is exactly the danger with making a deficit ratio the main goal. You can lower the deficit and still lose the larger fight for limited government.

The evidence points the same direction. Alberto Alesina’s research found that when countries had to repair their finances, plans built more on spending cuts generally performed better than those built more on tax increases.

Tax-based consolidations tended to be more recessionary. Spending-based restraint was more effective at stabilizing debt and less damaging to growth.

That should not be surprising. If you are trying to restore prosperity, you do not do it by punishing more work, saving, and investment. You cut spending.

The Fiscal Gap

By this framework, federal spending today should be at most $5.5 trillion, not above $7 trillion. Washington is overspending by roughly $1.5 trillion every year relative to a sustainable budget path. That is my estimate based on the official spending totals and the population-plus-inflation benchmark, and the direction is unmistakable.

The federal government has grown far faster than the country’s ability to support it.

Families Pay the Price

Families have been paying for that through inflation. The latest Consumer Price Index shows prices up 2.4 percent over the year in February 2026, with food prices up 3.1 percent and food away from home up 3.9 percent.

The PCE price index, which the Fed prefers, was up 2.8 percent over the year in January, with core PCE up 3.1 percent. Inflation is off its peak, but that is not the same as saying the damage is gone.

Families still feel it every time they buy groceries, go out to eat, or try to stretch a paycheck.

Debt and Distortion

The debt story is uglier still. The latest Congressional Budget Office outlook projects a federal deficit of $1.9 trillion in 2026, rising to $3.1 trillion by 2036. Debt held by the public rises from about 101 percent of GDP to 120 percent over that period. Net interest costs alone rise from $1.0 trillion to $2.1 trillion.

More and more of the federal budget will go simply to financing yesterday’s excesses.

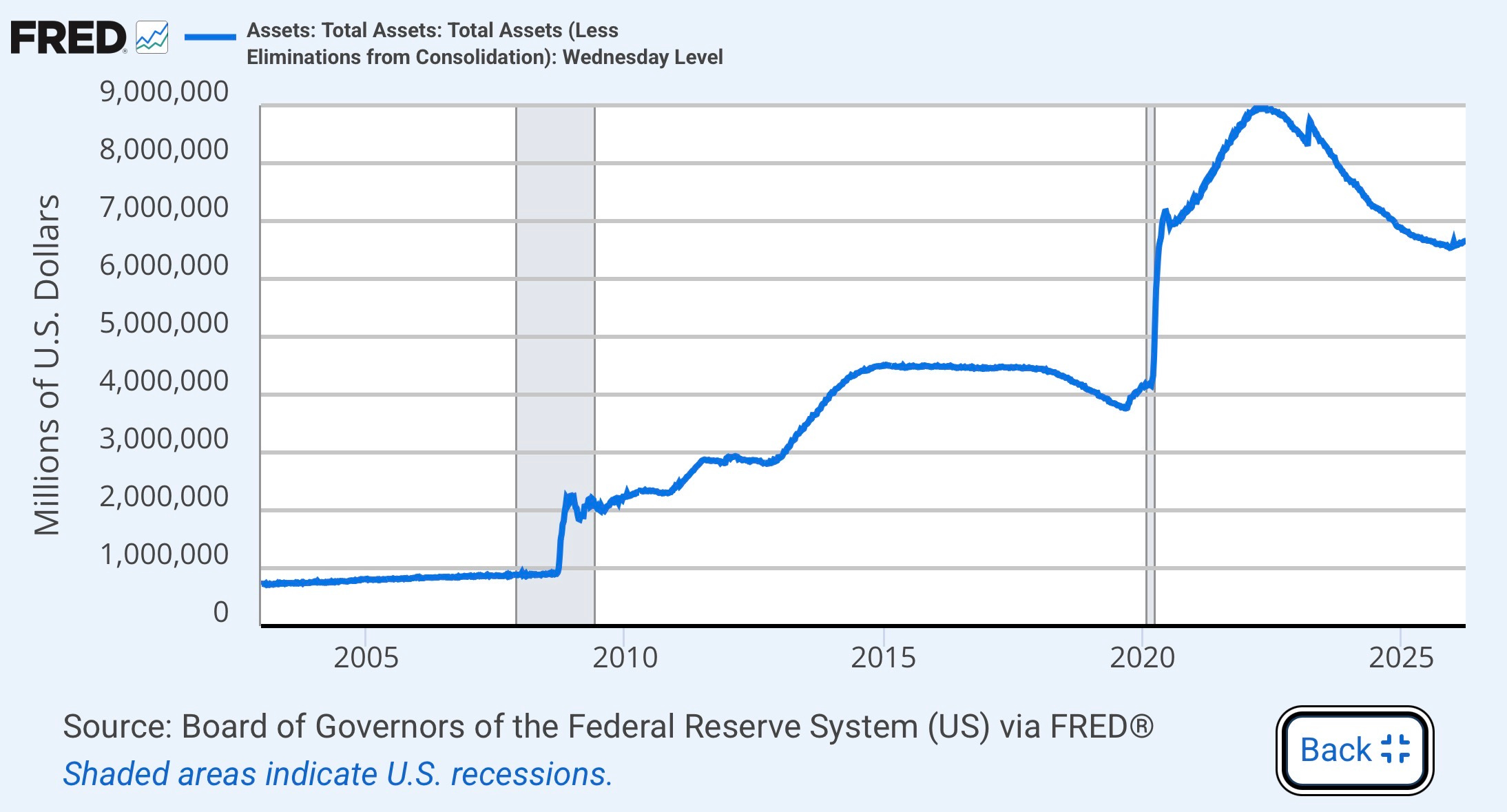

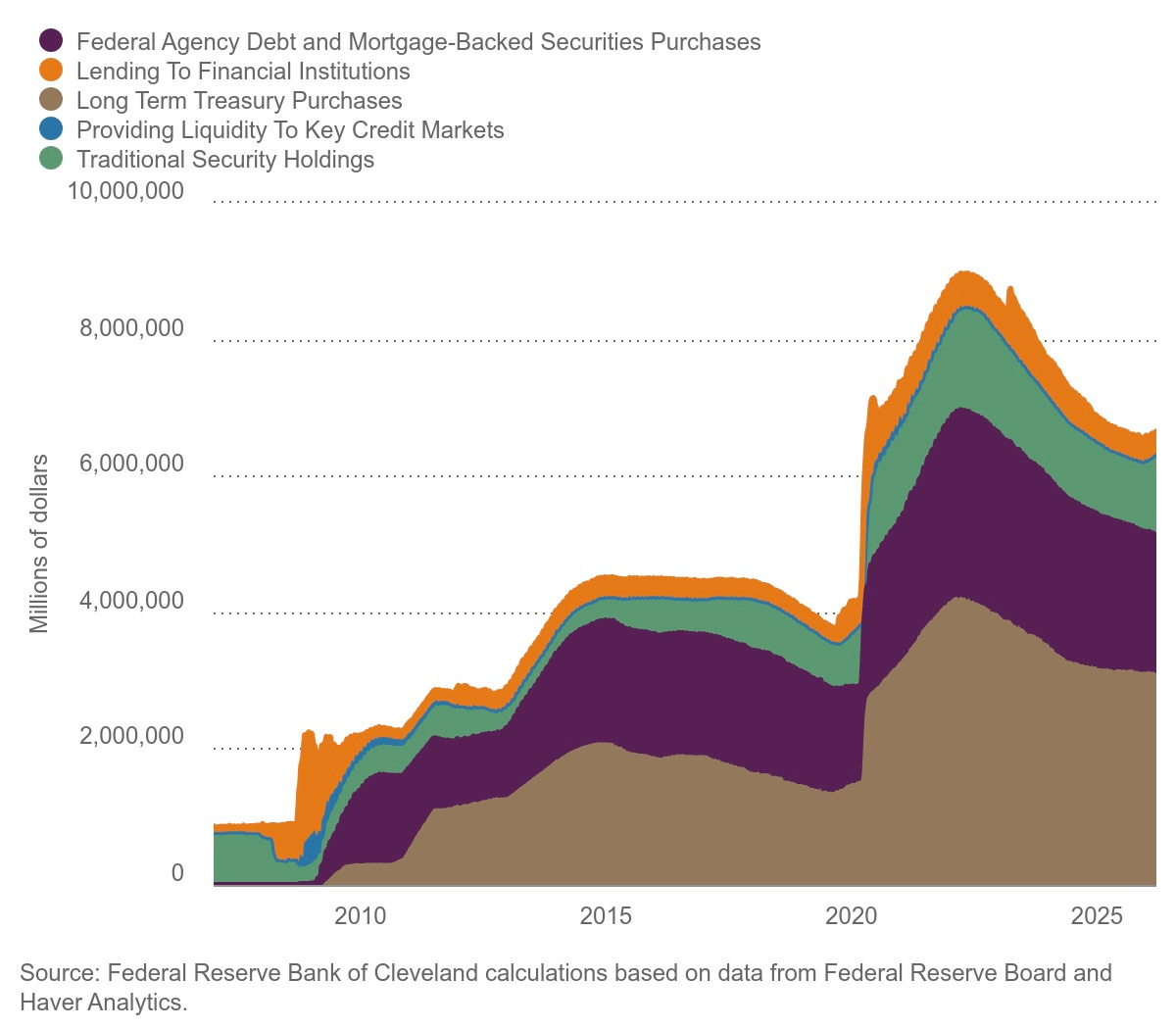

And then there is the Federal Reserve’s balance sheet. As of March 25, 2026, the Fed’s balance sheet of $6.7 trillion, including $4.4 trillion in Treasury securities and about $2. trillion in mortgage-backed securities.

The Fed’s own research shows that holdings like these put downward pressure on longer-term interest rates. In plain English, the central bank has helped make Washington’s borrowing binge look cheaper than it really is.

That error cannot last forever.

I do not know the exact form of the reckoning. It could come through higher long-term rates, weaker growth, renewed inflation pressure, or some ugly combination of all three.

But governments do not outrun arithmetic forever, and central banks do not permanently repeal market discipline.

Three Takeaways for Policymakers

1. A deficit target is better than drift, but it is not enough.

Use a 3 percent deficit-to-GDP goal as a warning light if you want. Use a spending limit as the steering wheel.

2. Spending is the real problem.

A hard cap tied to population growth plus inflation restrains government at its source and avoids the trap of trying to “fix” deficits with higher taxes.

3. Waiting is the dangerous choice.

With debt, inflation, and the Fed’s still-bloated balance sheet all pointing in the same direction, the prudent move is to shrink spending now before markets impose discipline later.

The Bottom Line

The federal government is too big. It spends too much. It borrows too much. And it has been shielded for too long by a central bank that softened the warning signs Washington should have been forced to confront years ago.

That cannot continue forever.

We should prepare now. Shrink government spending. Adopt a hard spending limit. Get our fiscal house in order while we still have a choice.

If this added value to your week, share it with a policymaker, staffer, journalist, or friend who should read it. Find more of my work at vanceginn.com and subscribe at vanceginn.substack.com.