Shutdown Theater, Debt Reality

Did you notice anything different? Contes should! Here’s why…

Hello Free Market Warriors!

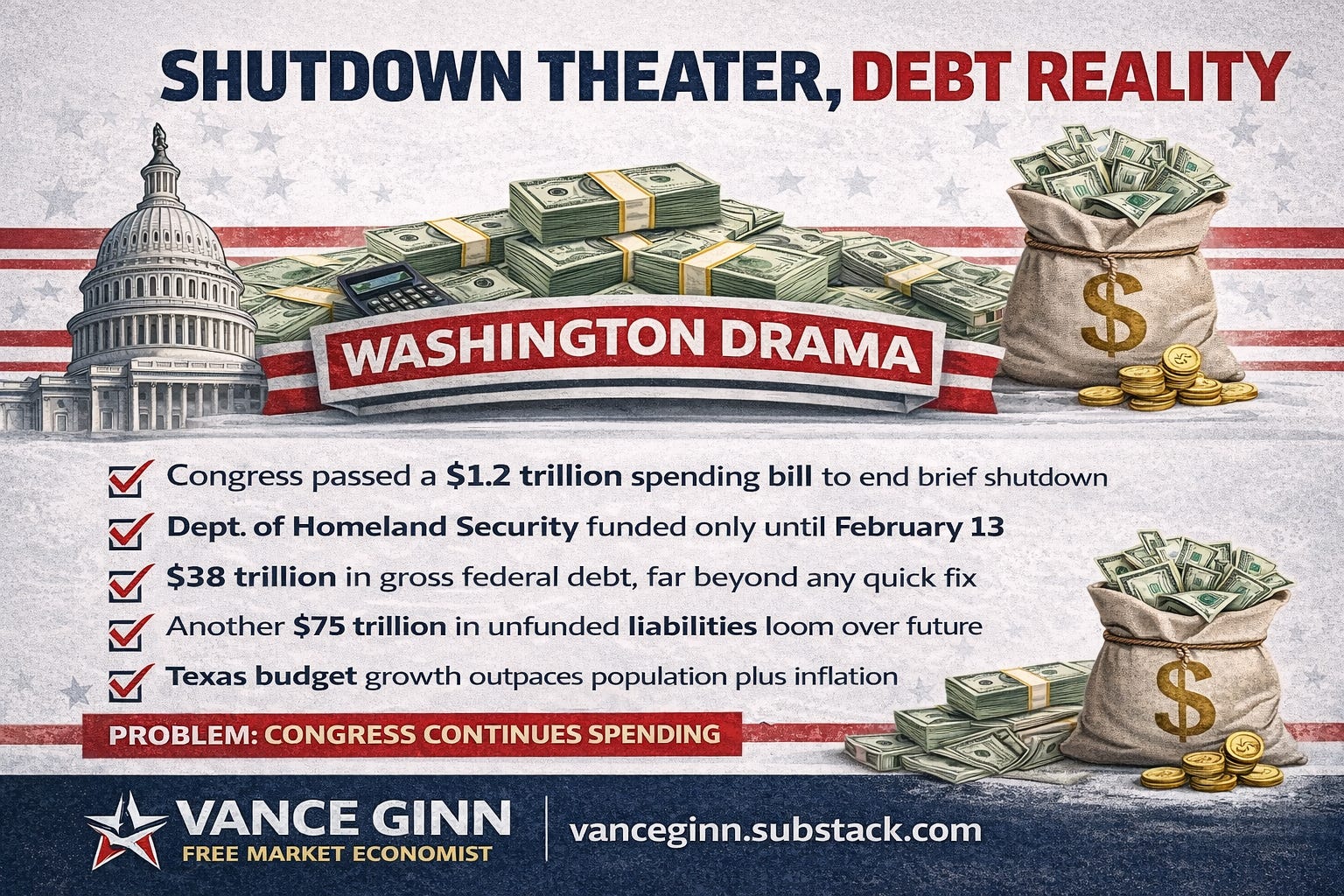

The federal government “shut down” at the end of January 2026, then reopened on February 3 after Congress passed a $1.2 trillion spending package that keeps most agencies funded through September. If you blinked, you probably missed the impact.

That is the point. For most families and businesses, daily life barely changed. Washington staged a high-drama budget fight, then “fixed” it with a giant bill and another deadline. Meanwhile, the real crisis keeps compounding: a federal government that spends too much, borrows too much, and relies on institutions like the Federal Reserve to absorb the consequences.

Congress ended the shutdown by passing an omnibus-style deal. The House vote was a razor-thin 217–214, and the bill included back pay for furloughed federal employees. That ended the second shutdown in four months, but it did not end the dysfunction.

The bill also left one massive loose end. The Department of Homeland Security was funded only through February 13, 2026, setting up another deadline that could trigger another lapse. That includes big, everyday functions like TSA airport screening, FEMA disaster response, and border and immigration enforcement.

The fight is now over whether Congress will attach new restrictions on DHS operations, with both sides already signaling they may force another showdown. You can read the basic structure of what agencies do during a lapse in the government’s own shutdown planning documents.

So what was accomplished?

A shutdown is not a spending cut. It is a temporary lapse in discretionary funding when lawmakers fail to pass appropriations bills. Discretionary means Congress votes on it each year. In contrast, mandatory spending like Social Security and Medicare largely runs on autopilot under existing law.

Even during a shutdown, many mandatory payments continue, many federal activities continue, and the federal government’s debt meter keeps running.

That is why a shutdown is mostly political theater. It interrupts some services, creates uncertainty, and turns federal workers into pawns. But it does not fix the budget, and it does not address the actual fiscal math.

The real fiscal math is ugly. The United States is carrying roughly $38 trillion in gross federal debt, which is the total amount of Treasury obligations outstanding. On top of that sits a mountain of unfunded liabilities, which is a polite phrase for promises already made for future benefits without dedicated funding set aside to pay for them.

People can argue about the exact size of those unfounded liabilities depending on assumptions, but the direction is unmistakable: the federal government has promised far more than it can pay without much higher taxes, major reforms, less spending, or significant inflationary financing.

Now connect that back to this shutdown “solution.” Congress kept most agencies funded through September. It might avoid a weekend of headlines, but it does nothing to slow the long-term spending trajectory that drives debt higher year after year.

And as debt gets bigger, interest costs become a budget-eater. When you owe $38 trillion, even small interest-rate moves matter. A one percentage point increase in average borrowing costs across a large portion of federal debt quickly translates into hundreds of billions more in annual interest expense over time.

That is money taxpayers send out the door before funding national defense, infrastructure, or tax relief. It is also money that crowds out private investment, because capital gets pulled into financing government IOUs instead of productive private activity.

This is why the Federal Reserve keeps getting pulled into fiscal failure.

When Congress will not control spending, markets start asking whether the Fed will be pressured to keep rates lower than they should be, or to buy more government debt to stabilize borrowing costs. That practice is often called monetizing the debt, meaning the central bank creates money to purchase government bonds. It can suppress rates in the short run, but it distorts markets and can contribute to inflation risks over time if money growth outpaces real economic output.

The Fed’s balance sheet is a major part of this story. A balance sheet is simply the Fed’s assets and liabilities, mainly the Treasury and mortgage bonds it holds, and the bank reserves it creates. Keeping that balance sheet huge can keep market signals muted and misprice risk. Shrinking it restores more market discipline, but it can also push some interest rates higher in the short run.

That is why Fed leadership matters, especially if the goal is to shrink the balance sheet toward something closer to historical norms, rather than living permanently in emergency-mode policy. If the Fed remains a quiet backstop for federal borrowing, Congress has even less incentive to make hard choices.

To be clear, “spending causes inflation” is too simplistic. Inflation is ultimately a monetary phenomenon: too much money chasing too few goods. But excessive federal spending absolutely pressures the Fed into choices that can amplify inflation risks, especially when deficits are persistent and political leaders want cheap financing. Fiscal irresponsibility and monetary distortion feed each other.

And this is not just a Washington problem.

Look at Texas as a warning sign. Texas does not have a personal income tax, which is a major competitive advantage. But spending discipline still matters, because spending is the ultimate burden of government. If spending grows faster than taxpayers can sustain, the bill shows up later through higher property taxes, higher sales taxes, or new fees.

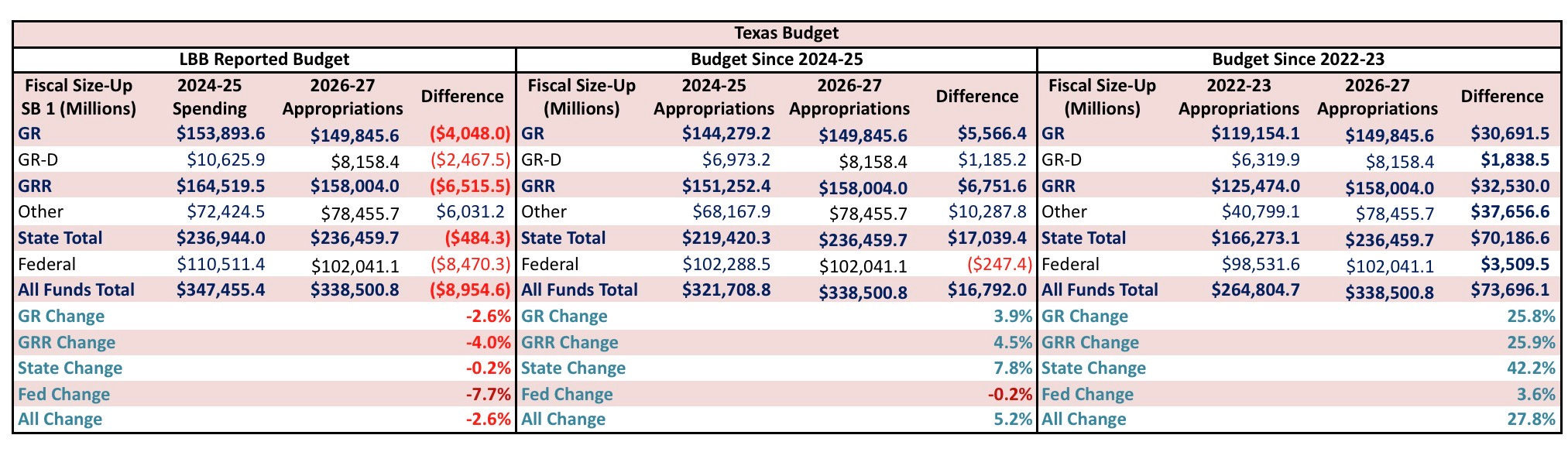

The Texas budget makes it clear that the budget is not declining using the Legislative Budget Board’s (LBB) fuzzy math. This is because the LBB is comparing spending to appropriations while there is no actual spending in the upcoming periods yet so the measurements aren’t consistent. Here are the results with consistent comparisons.

Since 2022–23, total state funds appropriations jumped from $166.3 billion to $236.5 billion, a rise of about $70.2 billion, or 42.2%.

Over the same period, all funds grew from $264.8 billion to $338.5 billion, up about $73.7 billion, or 27.8%.

Even just since 2024–25, state total rose from $219.4 billion to $236.5 billion, an increase of about $17.0 billion, or 7.8%.

General Revenue alone increased from $144.3 billion to $149.8 billion, up about $5.6 billion, or 3.9%.

A simple common-sense benchmark for sustainable budgeting is population growth plus inflation. If government grows faster than the number of people it serves and the cost of providing services, it is getting bigger in real per-person terms. That may be defensible if outcomes are improving, but it is rarely what happens. More often, it becomes the excuse for “we need more revenue,” meaning taxpayers pay now or taxpayers pay later.

That is the broader lesson from the shutdown episode. Republicans and Democrats can argue over line items, immigration riders, and which agency gets funded for how long. But the pattern remains: big spending packages, temporary patches, more debt, and another deadline.

This must stop. Congress needs fiscal hawks again, not performers. The federal government cannot keep treating budgeting like a recurring hostage situation while debt and interest costs compound. And states that claim to be different cannot keep spending like Washington and expect credibility to hold.

Closing

The shutdown ended. The headlines faded. The debt kept growing.

That is the reality Americans live with, even when Washington pretends everything is fine. If lawmakers want trust, they should stop governing by crisis and start governing by limits.

Restrain spending growth, pass sustainable budgets, and stop pushing the consequences onto the Fed and future taxpayers.

Review Summary

Congress ended the shutdown with a $1.2 trillion spending package that funds most agencies through September. The House vote was 217–214, and the deal included back pay. DHS funding only runs to February 13, keeping shutdown risk alive for major functions like TSA and FEMA.

The real crisis is the debt path, not the shutdown drama, with $38 trillion in gross federal debt and huge unfunded liabilities. Texas shows the same challenge at the state level, with state spending growth far outpacing a sustainable population-plus-inflation path.