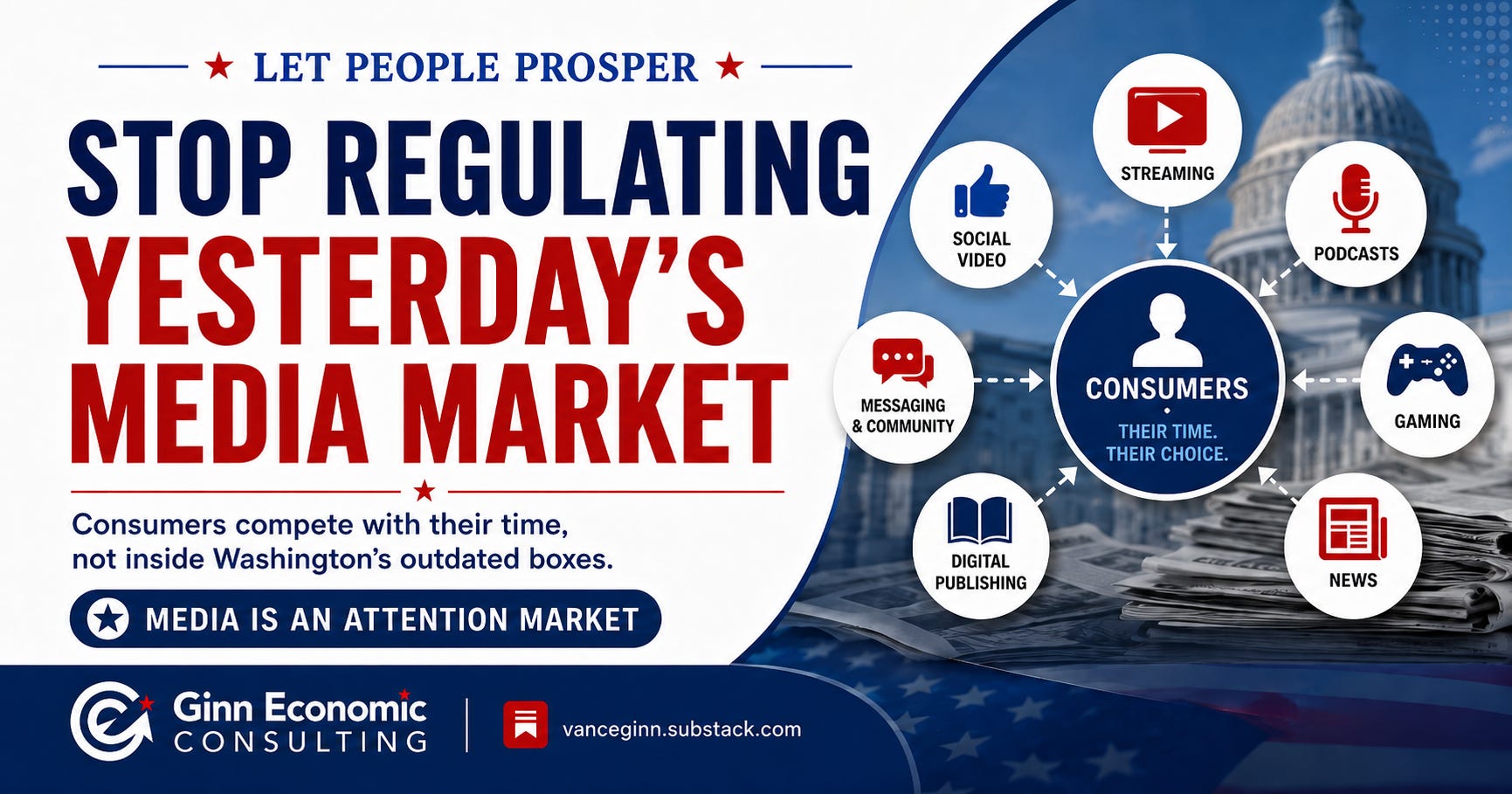

Stop Regulating Yesterday’s Media Market

Consumers compete with their time, not inside Washington’s outdated industry boxes.

Hello Friends,

Picture a family after dinner. One person watches Netflix. Another scrolls YouTube. Someone else plays a video game, listens to the Bible on Audible, or watches highlights from last night’s World Cup game.

Consumers see choices. Washington sees separate industries. That mistake matters because the government cannot protect competition when it misunderstands where competition occurs.

My newly published policy brief, A Consumer-Welfare Framework for Media Competition, Mergers, and Government Barriers, argues that modern media is an attention market. Streaming, broadcast, cable, social video, podcasts, gaming, music, sports, and news all compete for the same scarce resource: our time.

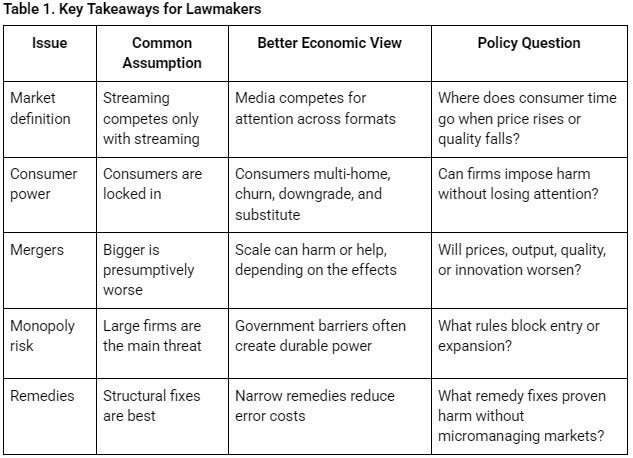

Three lessons should guide policymakers:

follow consumers’ attention rather than old industry labels,

require proof of consumer harm before blocking mergers, and

remove government barriers that protect established firms.

The first lesson is crucial because defining a market too narrowly can create on-paper monopoly power that does not exist in real life.

A Netflix series does not compete only with Hulu or Disney+. It competes with YouTube, TikTok, FC 26 game on PS5, a podcast, or simply going to bed. When one service raises its price or lowers its quality, consumers can cancel, downgrade, rotate subscriptions, or spend their time elsewhere.

The numbers confirm this. Nielsen found that streaming reached a record 47.5% of television viewing in December 2025, while broadcast and cable remained meaningful competitors. Parks Associates reports that 91% of internet households subscribe to streaming, households average nearly six video services, and traditional pay television still reaches 41%.

This is not a captive market. It is a crowded fight for attention.

Consumers also enforce limits. Deloitte found that 61% would likely cancel their favorite streaming service after a $5 monthly price increase. Popularity is not captivity.

That brings us to mergers. Politicians often begin with the wrong question: Is the company too large? The better question is whether consumers will face higher prices, less output, worse quality, or slower innovation. That is the consumer welfare standard, and it remains the best guardrail against turning antitrust into political industrial planning.

A merger can harm consumers, but scale can also spread costs, improve technology, combine content, expand distribution, and strengthen competition. Claims of “synergy” should be tested, not mocked. The government should follow the evidence rather than assume that bigger automatically means worse.

Over-enforcement carries real costs. Blocking a beneficial deal can reduce investment, eliminate an exit path that helps finance startups, and preserve legacy companies that consumers are already leaving. Media changes faster than government lawsuits move. By the time regulators finish arguing about yesterday’s market, consumers may have moved to tomorrow’s platform.

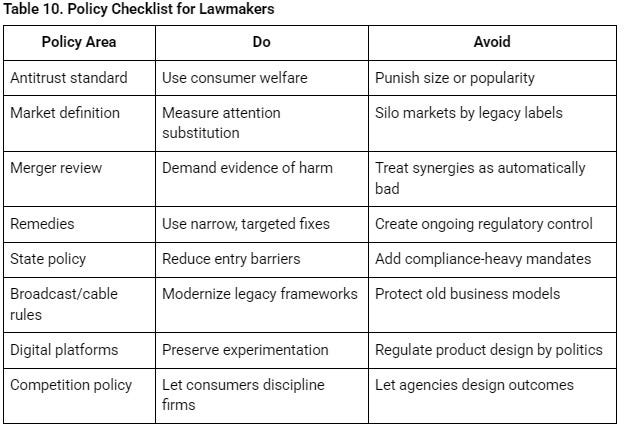

This builds on my recent report, Innovation Over Intervention. Antitrust should protect competition, not manage markets according to political preferences. The biggest threat to competition is often government.

Licensing rules, permitting delays, local franchise requirements, spectrum restrictions, liability exposure, and state regulatory patchworks raise the cost of entry. Large companies can hire lawyers and compliance departments. Startups and smaller creators often cannot. That is how regulations aimed at weakening incumbents can make them stronger.

The government should punish fraud and proven anticompetitive conduct. It should not punish success, protect outdated business models, or decide how many companies a market ought to have. Real competition comes from consumer choice, easier entry, and constant innovation. Media competition is bigger than any one merger. Policy should be, too.

Find more charts to quickly understand the paper in the full brief.

Thank you for reading,

Vance Ginn, Ph.D.

President, Ginn Economic Consulting